02 · The system

Axis · Wealthsimple Case

Axis is one system,

across every surface.

Not a feature. The connective tissue between client, advisor, and product.

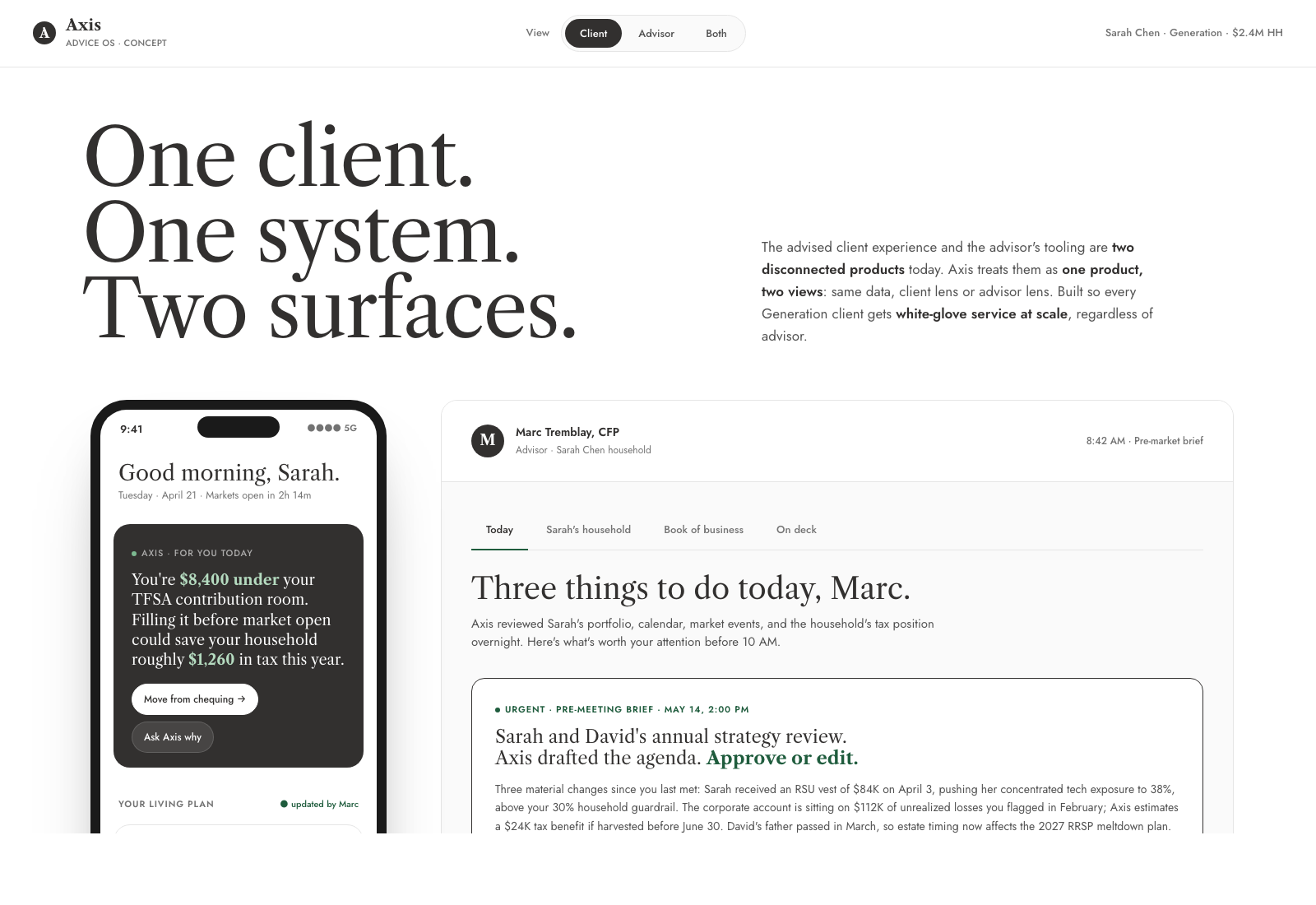

Surface 01

The Feed

Meetings & Tasks, re-ranked in real time. Ask any question; the feed re-ranks and explains.

Surface 02

The Living Plan

Financial Plan card. Updates as markets, tax rules, and policy shift. Ask what-if and see the impact.

Surface 03

The Pre-Meeting Brief

AI summary of recent activity before every advisor meeting.

Surface 04

The Membership Layer

Earned rewards tied to milestones and follow-through.

From the live prototype · two of four surfaces shown